Financial Planning for DIY Investors

Advice only, only when needed

No pitches to manage money

No financial product offers

No long-term commitments

When facing a big financial decision, a change in life circumstances, a career transition, or simply to establish a concrete plan.

When does a DIY investor need advice?

Services for DIY Investors

Who We Serve

DIY Investors

We serve clients across America from Highland Park, IL

Our Approach

Simple, Disciplined, Efficient

-

The foundation of your financial plan is built on spending projections and the strategies to fund that spending. Forming that foundation can initially seem daunting due to the numerous assumptions about future spending needs. We simplify the process by helping you clearly define and prioritize your goals, project the timing and level of spending, and tailor a funding strategy that works for you.

Many of us anticipate spending goals spread over decades, such as college tuition, discretionary spending on "bucket list" activities, living expenses during a sabbatical, basic needs in full retirement, and potential healthcare or long-term care expenses. We assist you in forming realistic assumptions about future spending, specifically how much you’ll spend and when. Based on these assumptions, we project spending cash flows over your goal horizon.

With a clear projection of your future spending goals, we can help formulate a funding strategy. Funding your projected spending can be achieved in various ways, whether from current income, borrowing, savings, insurance, or a mix of these sources. We can advise on securing the cheapest borrowing and aligning loan terms with your situation, such as borrowing to purchase real estate or to fund education. We also help develop savings strategies by evaluating savings patterns that align with your projected income. Additionally, we point out savings vehicles with tax incentives and low-cost investment options. For spending contingent on events like the need for long-term care, we might consider insurance solutions, which serve as a form of savings.

This process often requires multiple iterations. We evaluate different spending projections based on various assumptions and consider a range of funding strategies. It is time well spent, as it becomes the foundation of your financial plan. -

Our investment approach is guided by the following key principles.

Asset allocation. The first critical investment decision involves allocating your portfolio across major asset classes such as cash, bonds, stocks, and real estate. We recommend an allocation based on the time horizon for your spending goals and your personal preferences. We do not rely on "risk tolerance" surveys, as we believe in adjusting investing behavior to match your risk needs. For spending goals within the next ten years, we evaluate cash, bond funds, and bond ladders. For goals beyond ten years, we will consider stocks and real estate, but only if you have the need, willingness, and capacity to assume the risks. We generally favor a global stock allocation for maximum diversification and consider other factors like style and size, provided you are comfortable with the added complexity and committed to the long-term strategy.

Investment selection. With a target asset allocation in place, we typically recommend investing in diversified, low-cost mutual funds or ETFs that passively replicate market indexes. These options offer adequate diversification, low turnover, and low costs. We do not favor actively managed funds or individual stock selection due to the well-documented evidence that most managers cannot outperform market indexes over the long run after accounting for operating expenses and tax impacts.

Investment management strategy. We work with you to develop an investment strategy that you can adhere to in both normal and turbulent markets. Your behavior during market volatility will likely be the primary factor in your investment outcomes. We generally recommend formalizing an investment policy to maintain a regular discipline for rebalancing (or holding) and to promote rule-based actions that mitigate the negative effects of emotions during volatile financial markets.

To be clear, we do not believe in market timing in any form. Effective market timing requires accurately predicting the market's direction twice in succession: once to leave or enter the market and again to re-enter or leave. We believe this has a very low probability of success and can impose high costs when unsuccessful.

By adhering to these principles, we aim to create a robust investment plan that aligns with your goals and helps you navigate both stable and uncertain market conditions. -

Income taxes warrant special attention as it represents a large lifetime expense. Not only is the tax code complex, but it frequently changes through updates to federal and state tax law. Moreover, taxes affect most financial transactions both in the current year and potentially far into the future. For these reasons, we prioritize helping you minimize your tax burden through a comprehensive, lifetime planning approach.

Immediate tax opportunities. First, we raise awareness of adjustments, deductions, and credits that could apply to your situation, starting with clear-cut opportunities that don't rely on assumptions about future income levels or tax rates. These are the lowest-hanging fruit, often easy to overlook.

Income deferral strategies. Taking a lifetime view, we evaluate opportunities to defer income recognition using vehicles such as IRAs, company 401(k), 403(b), and 457 plans. Crucially, for any income deferrals, we ensure you have a strategy for future income recognition to avoid unwelcome tax surprises down the road.

Investment tax efficiency. We assess strategies to minimize the tax impact on your investment returns. Guided by your holistic asset allocation, we support decisions on placing investments among taxable, tax-deferred, and tax-free accounts. Additionally, we evaluate strategies for opportunistically realizing gains or losses, commonly known as tax-loss harvesting or gain harvesting. While highlighting the potential benefits, we also counsel on execution risks and whether the benefits justify the effort.

Business tax planning. If you are thinking about starting a business or already own a business, we can evaluate your business plans, establish sound bookkeeping processes, and minimize your tax burden.

By addressing these key areas, we aim to help you effectively manage and reduce your tax expenses, ensuring a more secure financial future. -

A holistic risk management discipline is essential to your financial plan. Rather than aiming to eliminate all risks, it focuses on identifying opportunities to reduce risk or to retain and manage risk when appropriate. Your risk appetite will guide the rest of your financial plan, including investments, insurance, and estate planning.

Identifying risk exposures. First, we help identify all forms of risk to your financial strength. These include insurable risks like accidents, morbidity, mortality, and longevity; investment risks such as credit and market risks; information security risks; and plan continuity risks.

Assessing risks and opportunities. After creating an inventory of risk exposures, we assess both potential losses under adverse scenarios and opportunities under extreme yet favorable scenarios. We generally prefer forming and evaluating “what if” scenarios over interpreting probabilistic results from Monte Carlo simulation models. Given our extensive experience in risk management and stochastic analysis, we are cautious about relying on Monte Carlo simulations, especially for multi-decade projections.

Managing risk. After a thorough assessment of risk exposures, we recommend techniques to manage risk. This involves reducing or eliminating certain risks and retaining or increasing others when the risk/reward balance is favorable. For retained risks, we formulate plans for loss mitigation and recovery under adverse events. We encourage formalizing risk policies to guide behavior and mitigate the effects of emotions during extreme scenarios.

Continuity planning. Because our clients are hands-on with their finances, we emphasize the importance of continuity plans for managing your finances in the event of incapacity or premature death.

By incorporating these principles, we aim to provide a comprehensive risk management strategy that aligns with your overall financial goals and ensures a secure financial future. -

We will consider insurance products to reduce or eliminate insurable risks based on your risk management decisions. We advocate using insurance to mitigate catastrophic losses due to accidents, theft, disease, disability, incapacity, premature death, or personal liability. Except in specific estate planning situations, we generally do not recommend insurance products as investment vehicles for funding savings goals or managing market risks due to their complexity, illiquidity, and hidden fees.

For health insurance, we can help you assess plans offered by your employer or from the Marketplace. If you own a business with a partner or employees, we collaborate with trusted brokers to identify options for group insurance plans.

For property and liability insurance, such as home, auto, and business insurance, we help determine the appropriate coverage amounts and levels of loss sharing, such as deductibles. We recommend re-evaluating product offerings with your insurance agent every 2-3 years.

For long-term insurance needs like life insurance, disability income insurance, or long-term care insurance, we work directly with brokers to find the simplest and most affordable products offered by highly-rated insurance companies. In addition to selecting products, we help determine the proper size and duration of coverage for your needs. We generally do not recommend annuities due to their complexity, high fees, and lack of inflation indexation. If you own any life insurance or annuity policies, we will evaluate their appropriateness for your long-term needs and advise on strategies for managing, replacing, or lapsing the policies. -

Planning gifts and your estate are critical yet often overlooked components of a financial plan. These topics can be challenging to discuss and may require difficult decisions. We can help you navigate these issues within the context of your overall financial plan, always collaborating with an attorney who is licensed in your state and who specializes in estate planning and administration.

Charitable and family giving. First, we can help you maximize your charitable giving or gifts to family and friends while you are alive. We optimize your gifting strategy with techniques that minimize income and gift taxes. We also coordinate your gifting strategy with your estate plan to minimize gift and estate taxes at both the federal and state levels, if applicable.

Health and property directives. Second, through a referral or direct collaboration with an attorney, we guide you in establishing the legal documents that can speak for you, or appoint someone to speak for you, on matters of health and property if you become incapacitated. We encourage you to establish healthcare directives, such as a Power of Attorney (POA) for health care and a living will, and a Power of Attorney for property to manage your finances if you are unable to do so.

Wills and trusts. Third, through a referral or direct collaboration with an attorney, we help you establish the legal documents, such as a will and living trusts, to ensure your assets are transferred upon your death according to your wishes in an orderly and cost-efficient manner. This can help avoid the costly and time-consuming probate process. Although your documents should be prepared and executed by a licensed attorney specializing in estate planning and administration, we coordinate the process and ensure your estate plan aligns with the rest of your financial plan.

By addressing these key areas, we aim to provide a comprehensive and integrated approach to your financial plan, ensuring your wishes are honored and your loved ones are taken care of.

The Process

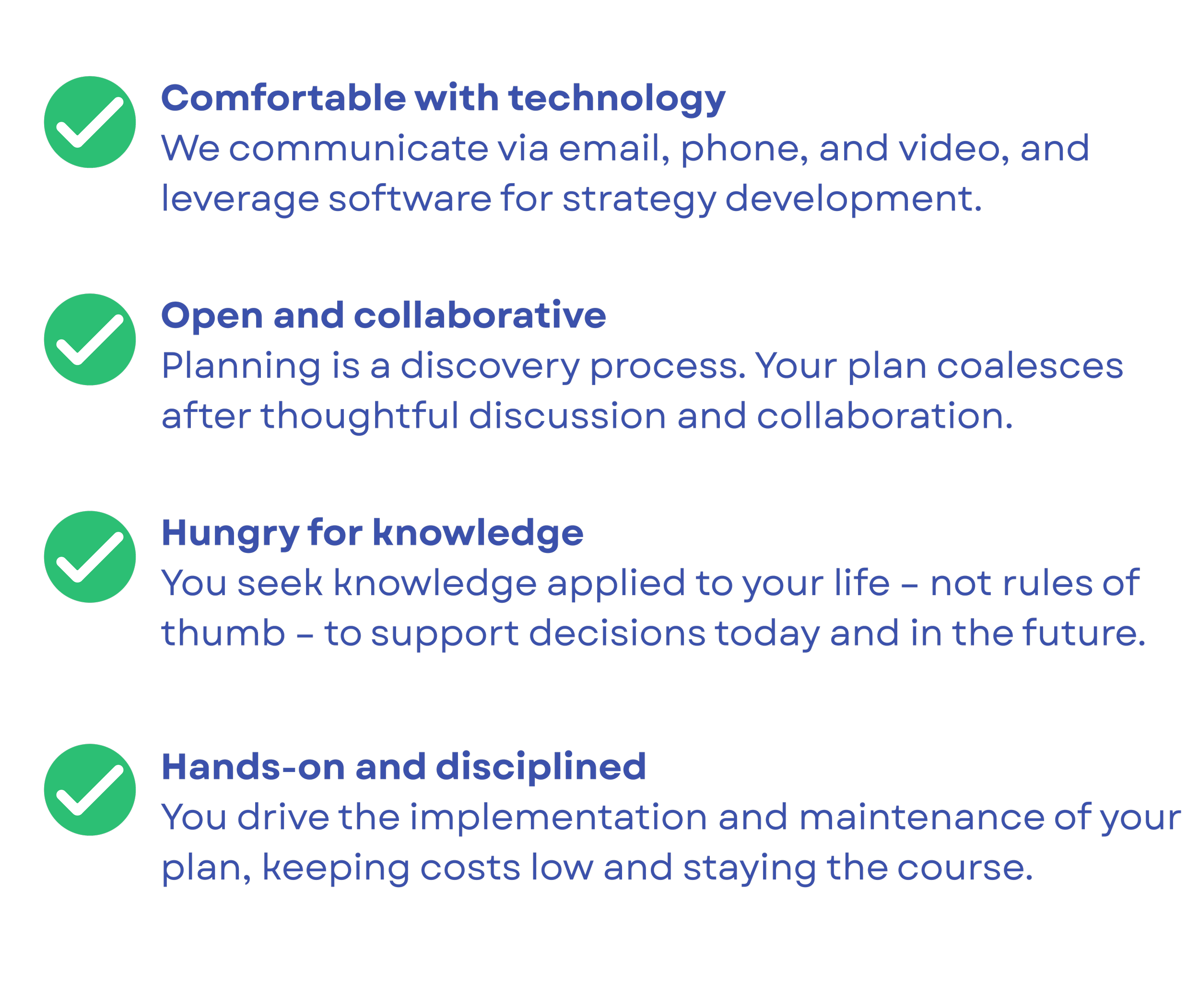

Our process is collaborative

We take time to confirm a fit, and then collaborate closely to develop your plan.

FAQs

-

Yes, we serve clients across the country through phone, video meetings, and email.

-

Yes, if you prefer, we can arrange to meet at a co-working space or at your office, but please note, I charge my hourly rate for commuting time.

-

Yes, you are welcome to schedule future check-in meetings as needed, by the hour (no minimums).

-

Though we have no minimums, we must establish context and carefully consider alternatives, which typically takes more than an hour.

-

Electronic funds transfer or credit card.

-

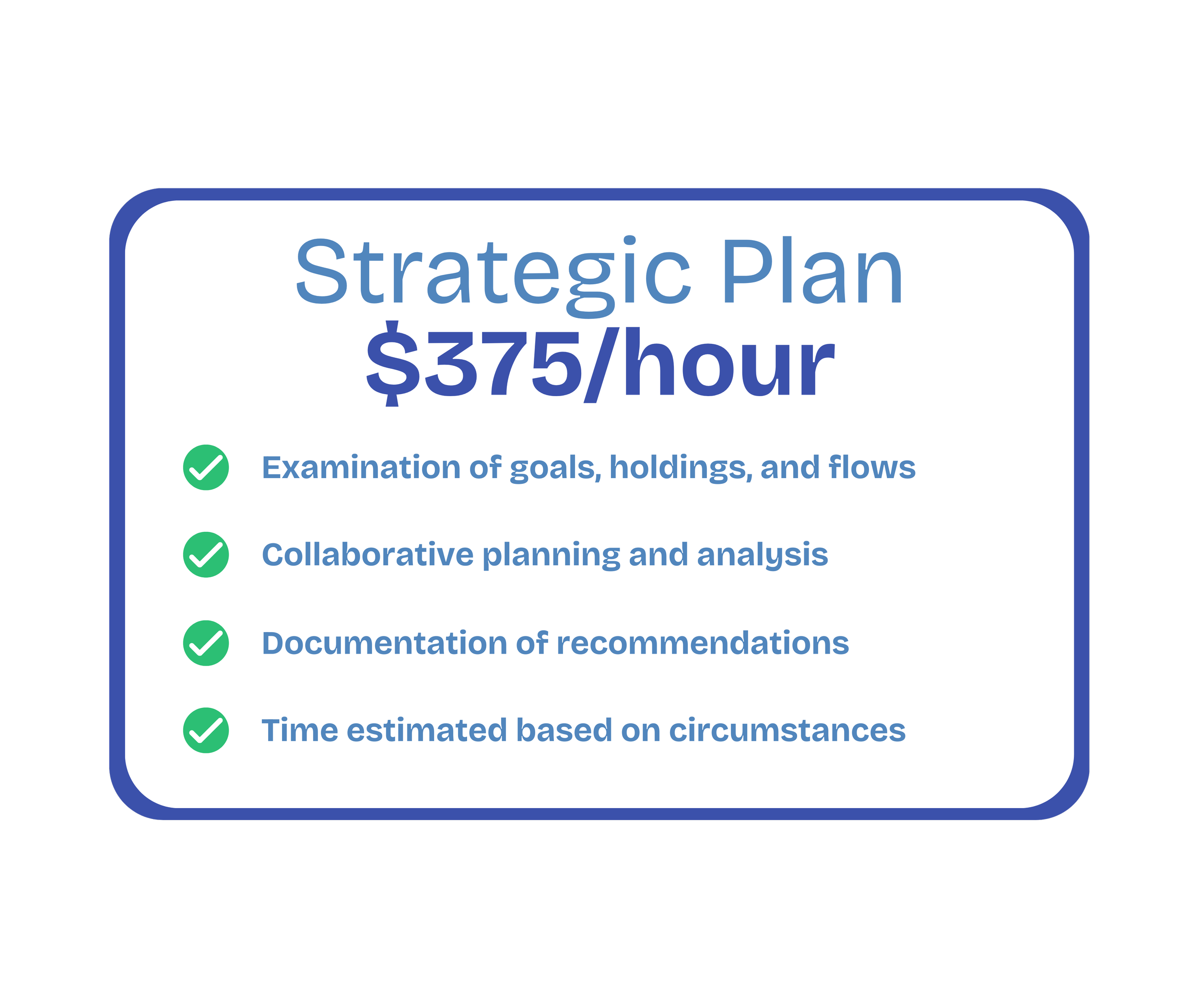

If you are a DIY accumulator with well-defined goals and organized records, the Financial Review is likely sufficient. Otherwise, a Strategic Plan would be appropriate. We will assess during the discovery call.

-

We do provide tax advice, however we do not prepare tax returns. We will recommend user-friendly tax preparation software or we can refer you to a tax preparation service.

-

We offer advice only, that is, we do not manage investments or otherwise implement plans. However if desired, you can share your computer screen with us, and we will answer questions live as you take the steps to implement your plan.

-

We ask you to scrub documents of any social security numbers, account numbers, driver's license numbers, or any other personally identifiable information. We exchange documents through a file vault.

-

This outcome is highly unlikely. Our top priority is client satisfaction. We will evaluate a fit during the initial call. If we have any doubt about delivering value to your satisfaction, we will refer you to other advisors.

More Questions?

About

Brian Rhoads, CFA, EA

-

Location: Brian, a lifelong Illinois resident, grew up in rural Oregon, Illinois. After graduating from Augustana College in 1997, Brian settled in the northern suburbs of Chicago where he remains – at least until another Chicagoland winter gets the best of him.

Family: As luck would have it, Brian met his future wife, Mary, while on a daily train commute. Many commutes later, Brian and Mary tied the knot and eventually settled in Highland Park, Illinois, where they have been raising their son and daughter, now in their late teens.

Free time: In addition to spending time with family at home and traveling around the world, Brian jogs the Green Bay Trail, cycles throughout Lake County, volunteers as a tax preparer, and continues searching for a reliable golf swing. Brian remains a loyal fan of the Chicago professional sports teams, and still reminisces about the '85 Bears. -

Brian started Checkpoint Financial Planning, LLC to bring personalized financial advice to more people across the country. Brian observed that many people intentionally manage their own money and finances, yet still need professional financial advice from time to time, but without strings attached. That is, they do not want to pay an advisor an on-going fee to monitor their investments, face pressure to buy an annuity or life insurance, or commit to an on-going subscription service. Rather, these people just seek unbiased, independent financial advice when needed.

To be clear, Brian is not crusading against advisors who manage investments, insurance and annuity brokers, or advisors offering subscription services. Indeed, some people need such services or products, and in those cases, Brian will refer those people to advisors who would be a better fit. -

A math enthusiast at heart, Brian steered his education towards the applications of mathematics in the fields of economics and finance.

Undergraduate: Brian earned his bachelor's degree, summa cum laude, from Augustana College with concentrations in mathematics, economics, and finance.

Graduate: Early in his professional career, Brian earned a master's degree in financial mathematics from the University of Chicago, which provided an advanced quantitative foundation for evaluating risk and return in the financial markets. -

Brian earned professional credentials in investments (CFA®) and income taxation (EA):

Chartered Financial Analyst (CFA®): Brian was awarded a CFA charter by the CFA Institute after passing three examinations covering a wide range of investment topics, including ethical and professional standards, fixed-income analysis, alternative investments, derivative investments, portfolio management, and wealth planning. As a CFA Charterholder, Brian must abide by the CFA Institute Code of Ethics and Standards of Professional Conduct.

Enrolled Agent (EA): Brian earned the Enrolled Agent credential, the highest credential awarded by the Internal Revenue Service (IRS), after passing a three-part exam covering individual and business income tax returns. As an Enrolled Agent, Brian has the ability to provide tax advice and represent taxpayers before the IRS, and must adhere to ethical standards and complete 72 hours of continuing education courses every three years. -

Brian's professional experience in the financial services industry spans 28 years. Brian is immeasurably grateful for the relationships with his colleagues and clients over the years.

At Quantitative Risk Management (QRM) for 23 years, Brian provided consulting services to life insurance companies and commercial banks on a range of topics including asset/liability management (ALM), financial planning and analysis (FP&A), portfolio optimization, capital management, stress testing and contingency planning. While at QRM, Brian developed expertise in the tools and techniques for aligning investments with liabilities, measuring and managing financial risks, and developing dynamic investment strategies.

At Allstate Insurance Company for 4 years, Brian priced personal auto insurance in the property & casualty company for 2 years, and then managed interest rate risk and liquidity risk for Allstate's life insurance subsidiaries for another 2 years. In these roles, Brian gained valuable knowledge of the insurance industry and insurance products including life insurance, annuities, property insurance, and liability insurance products.